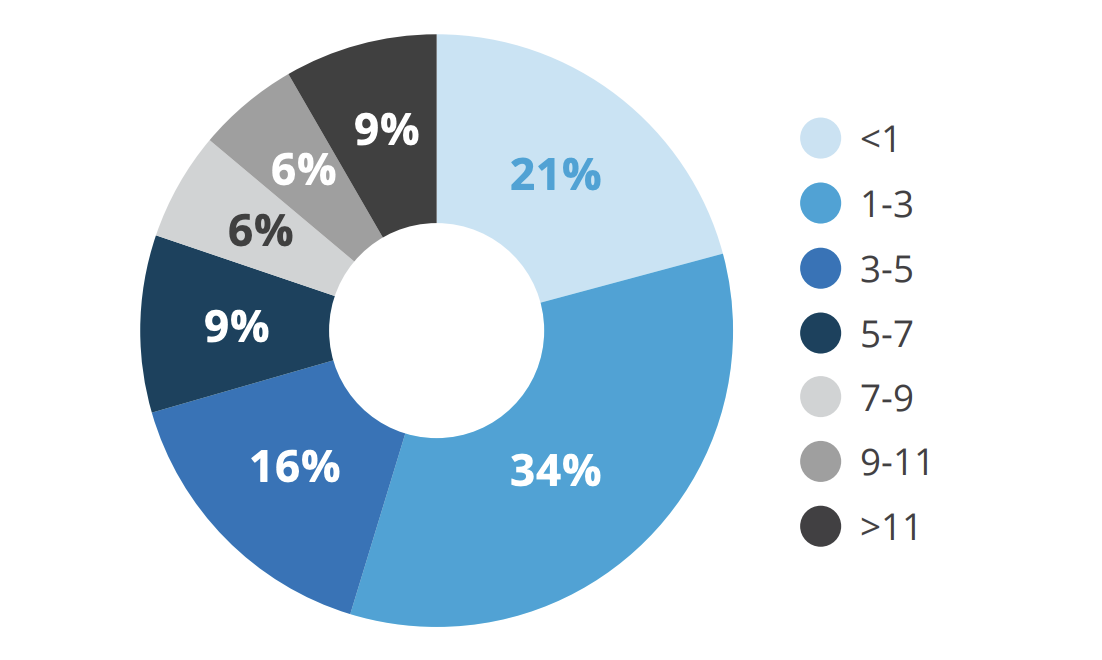

Figure 1: Leverage ratios of 340 blended finance transactions

With the annual financing gap for the Sustainable Development Goals (SDGs) rising from $2.5 trillion to $4.2 trillion in part because of the impact of the COVID-19 pandemic on developing economies, the use of catalytic capital from public or philanthropic sources to increase private sector investment in developing countries is one critically important approach to mobilizing new sources of capital for the SDGs. With annual blended finance flows currently far below what is needed to achieve the “billions to trillions” agenda, leverage ratios can help determine how effective concessional capital (i.e. capital priced below market terms) has been within blended finance transactions to date. Leverage ratios are defined here as the amount of commercial capital mobilized by each dollar of concessional capital, where commercial capital includes capital deployed by private, public (e.g., Multilateral Development Banks (MDBs) and Development Finance Institutions (DFIs)) and philanthropic investors at market rates.

This Brief updates a study published by Convergence in 2018 that benchmarked leverage ratios for a sample of 72 blended finance funds. The study found that, on average, blended finance funds have leveraged $4 of commercial capital for every dollar of concessional capital, with only a fraction of this commercial capital ($1.10) coming from private sector investors. This Brief expands the universe of transactions under study to 340, including transactions structured with blending archetypes other than concessional debt and equity, like guarantees and technical assistance. The Brief found that the average leverage ratio for blended finance transactions remains in line with what was recorded in 2018, at 4.1. The stagnancy of the leverage ratio could be explained by the fact that donors have not prioritized and budgeted private sector mobilization as a necessity to significantly narrow the SDG financing gap, and the size distribution of blended transactions remaining constant.

This Brief also examines ‘private sector mobilization’, which refers to the amount of commercial capital, specifically from private sector investors, that has been leveraged by concessional capital. The average private sector mobilization ratio has been 1.8, suggesting that just under half of the commercial financing mobilized by each dollar of concessional financing has come from private sector sources, with the remainder coming from MDBs/ DFIs and philanthropic investors. In other words, at present concessional financing is most often being blended with commercial capital from MDBs / DFIs, rather than supporting third party private sector mobilization.

Here are some key takeaways from the Brief:

Average leverage ratios are highest in LatAm and lowest in Global and East Asia: Average leverage ratios were highest in Latin America and the Caribbean (4.7), while transactions targeting Global (3.1) and East Asia and Pacific (3.0) recorded the lowest average leverage ratios. Latin America remains a popular area of interest for blended finance practitioners, with just under half (47%) of the fundraising transactions showcased on Convergence’s deal-matchmaking platform targeting the region. Average private sector mobilization ratios were highest in South Asia (2.1), Latin America and the Caribbean (1.8), and Sub-Saharan Africa (1.8), but private capital as a proportion of total commercial financing leveraged was highest for transactions targeting Global (1.7; 56%) and East Asia and Pacific (1.6; 53%). That is, blended transactions targeting these regions mobilized levels of private capital near the average (1.8) but closed with less subsidization of public institutions. This suggests that in other regions, the presence of DFIs / MDBs may be needed for deals to close, or that their presence may be crowding out private sector capital.

Figure 2: Average leverage ratios (light blue) and private sector mobilization ratios (dark blue) by target region(s).

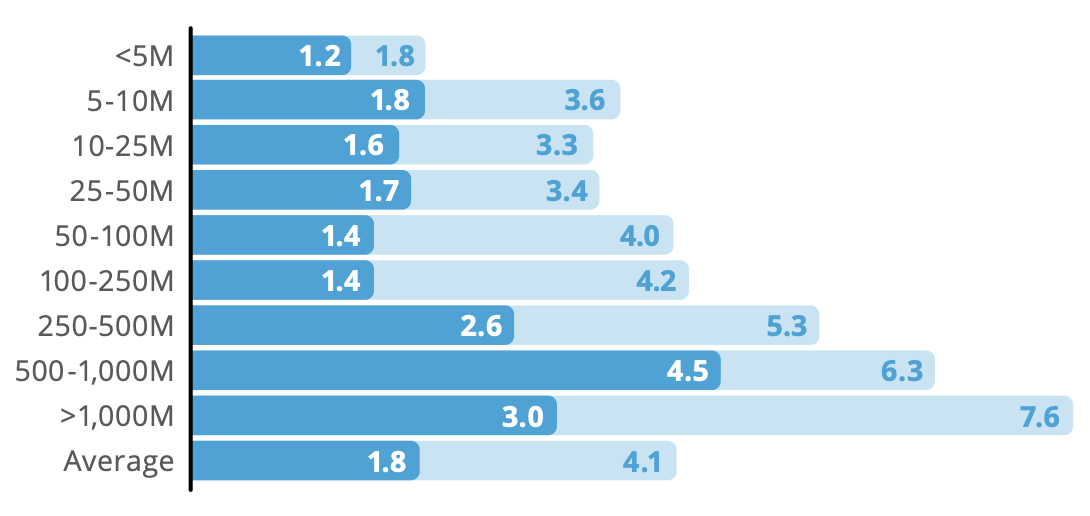

Larger transactions mobilize more commercial capital on average: Larger blended transactions have leveraged higher amounts of commercial capital per dollar of concessional funding, with average leverage ratios almost perfectly increasing with transaction size through to the $1 billion plus range, where average leverage ratios reach 7.6. Convergence has long made a case for launching proven and replicable blended finance structures and aggregation vehicles, given their appeal among private sector investors. Indeed, private capital as a proportion of total commercial capital leveraged has been highest for transactions in the $500-1000 million range (4.5; 70%). Institutional investors have significant assets under management (AUM) and need large deal sizes to avoid the high transaction costs associated with considering multiple smaller deals. There is, however, an interesting pattern at the other end of the scale. PE / VC firms and corporations have been active in very small transactions, with the private sector being the critical source of commercial funding in the <$5 million range (1.2; 65%). DFIs / MDBs have largely been absent in direct deals at this end of the spectrum.

Figure 3: Average leverage ratios (light blue) and private sector mobilization ratios (dark blue) by deal size

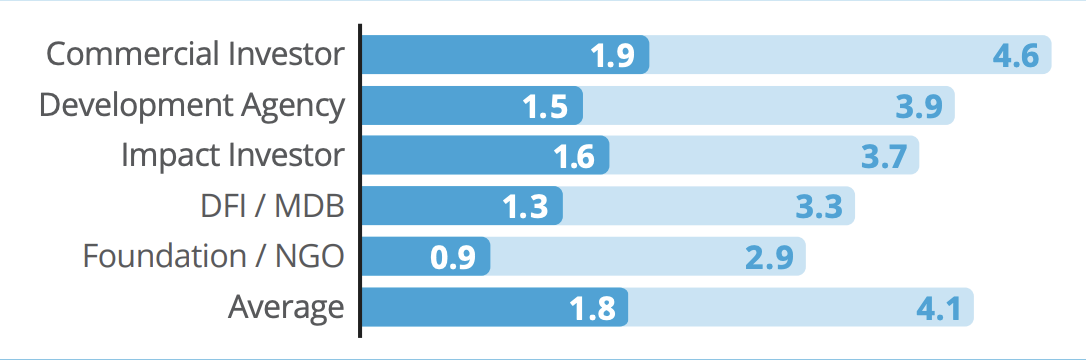

Commercial investors originate deals with high leverage ratios: Blended transactions originated or led by commercial investors (4.6) have had the highest average leverage ratios on average, followed by development agencies (3.9) and impact investors (3.7), while those originated or led by foundations / NGOs (2.9) have had the lowest. Foundations / NGOs as deal sponsors have also mobilized the smallest amount of private capital as a proportion of commercial financing leveraged (0.9 average private sector mobilization ratio; 29% of commercial financing leveraged). Private sector mobilization is not often an express goal of foundations; leveraging additional capital has been identified as one of five uses of catalytic capital, including facilitating innovation and safeguarding impact. Meanwhile, commercial investors (1.9; 42%), development agencies (1.5; 38%), and impact investors (1.6; 44%) as deal sponsors have mobilized similar amounts of private capital as proportions of commercial financing leveraged.

Figure 4: Average leverage ratios (light blue) and private sector mobilization ratios (dark blue) by deal sponsor type.

To move away from blending concessional capital with commercial capital from DFIs / MDBs and towards effectively mobilizing private sector investment, donors will have to become more strategic, by Increasing the amount of ODA they allocate to private sector mobilization, instituting KPIs within DFIs/MDBs that reorient them towards private sector mobilization and providing more data on the financial terms and ex-post development impact of their transactions.

Become a member and read the full brief.